Auto Parts Retailers [$AZO, $ORLY, and $AAP]

Right Parts, Right Place, at the Right Time

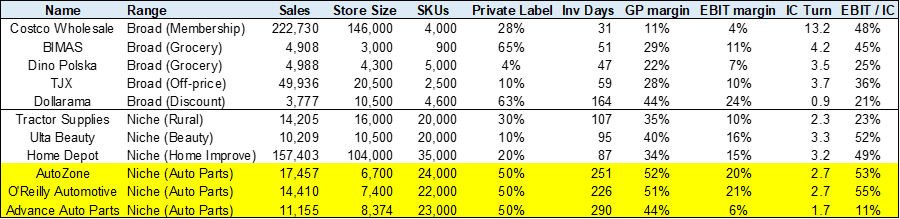

Retail is tough. There is no secret to this industry. Everyone walks into your store and sees your layout. Retail virtually has no entry barrier once you get location and supply, and there usually are plenty of malls and vendors. What I see as the finesse of retail execution often revolves around some ideas of combining lean cost structures (low margins), streamlined SKUs, and fast inventory turns. Costco is often touted as the prime example with its massive ~146K Sq ft stores having merely 4000 SKUs (Walmart per store sales is 1/3 but 30x in SKU), and 10% GP Margins that no one else could match, generating loyal member retention rate of >90% as well as a mouth-watering pre-tax returns on capital upwards of 40%. If you sell at lower margins, you hope that you are compensated with streamlined SKUs and better IC turns with lower working capital. This works for stores that sell a broad range of goods efficiently.

Auto stores, being niche retailers, are nothing like Costco. Stores are generally small (7,000 sq ft), GP margins are high at 50%, stores carry 22K SKUs with over 200 days on inventory and EBIT / IC reaches 50%. Here the opposite happens. Slower inventory turn must be carefully managed to avoid low IC turn, while accompanied by higher margins, to achieve a stellar return profile.

Since retail is all about space utilization, to juice up the efficiency for each square feet used, we can either sell a small selection of goods with low pricing at high velocity, or command high margins from instant availability, more private label goods, and excellent in-store services. It’s fine to have low inventory velocity, as long as for each sale its higher margin well compensating and offsetting working capital needs with long supplier days.

Auto retailers serve two customers who need car parts to fix a broken car: Do-it-yourself (DIY) and Do-it-for-me (DIFM) (aka commercial/professional) customers. DIY customers are car owners who prefer to fix cars by themselves, and DIFM customers are the owners of car garages/repair stores/body shops looking for parts replacement to complete a repair job.

Since America lacks a comprehensive public transport system especially in its rural areas, cars are the default indispensable traveling tool, and a broken car is an immense trouble. Hence, auto parts stores are set up to take advantage of this inconvenience as a gateway to get the broken car fixed as soon as possible. It turns out the stores are not just selling the parts, but also the customer service and the speed which they offer the parts that is the main reason why they fetch >50% GP margins. I said everyone walks into your store and copies your layout, but one cannot easily copy your backend logistics infrastructure. So, the whole mental model of the business comes down to how to efficiently deliver these parts to customers as soon as possible. Distribution networks are the strong barriers set up by incumbents in the auto parts industry that are hard to replicate.

Like an emergency pharmacy store, a typical auto part shop mostly sells items that are needed to fix the car. About half of the stuffs sold in a typical AutoZone store are related to car failures (Engines, Compressors, Fuses, Clutches), while the remaining half is split into 35% of maintenance items (Brakes, Oil, Spark Plugs, Refrigerants) and only 15% discretionary items (Wax, Air Refresher, Mirrors). Tires are not sold in auto part stores. A car won’t work without fixing such failure parts and the maintenance items are regular top-ups as when needed. So, each store carries about 22-24K SKUs, and the share of inventory distribution is heavily skewered towards the storefront (>80%) rather than distribution centers and hub stores1.

Auto stores would sell OEM (made by the same car producer), remanufactured (recycled old/damaged parts), and aftermarket parts (made by someone else other than OEM). But the preference really comes down to each customer. OEM parts are seen as having higher quality than aftermarket parts and appeal to customers with premium brands such as BMW and Mercedes. For example, a brake pad may cost somewhere around $50-150 for OEM brands but starts at $20 for aftermarket. Well, categories matter too, with failure and engine parts leaning towards OEMs since the precision of their manufacturing mold matters more to fit perfectly, but more aftermarket maintenance parts and tools sold.

Auto stores have half of the sales in private label that typically come with better margins. Battery is the most common store brand sales, with Advance Auto Parts’ Diehard brand (Yes, they got Bruce Willis from the movie to shoot its commercial) reaching $1B in sales in 2022 and pushing its private label over 50%. Likewise, AutoZone also has >50% sales in private label according to Morningstar, with Duralast/Valuecraft (battery), SureBilt (wrenches) and ProElite (car wash) being the popular brands. This similarity in high private label penetration across all 3 players is no coincidence, as private label items usually come with juicer margins with greater control from retailers on pricing and higher share of profits without the layer compensated to OEM suppliers. O’Reilly has deliberately increased its private label share from 25% in 2007 to 50% in 2022, with its Super Start (battery), Import Direct (brake pads), Master Pro (lubricants) and Power Torque (wrenches) being the more popular ones.

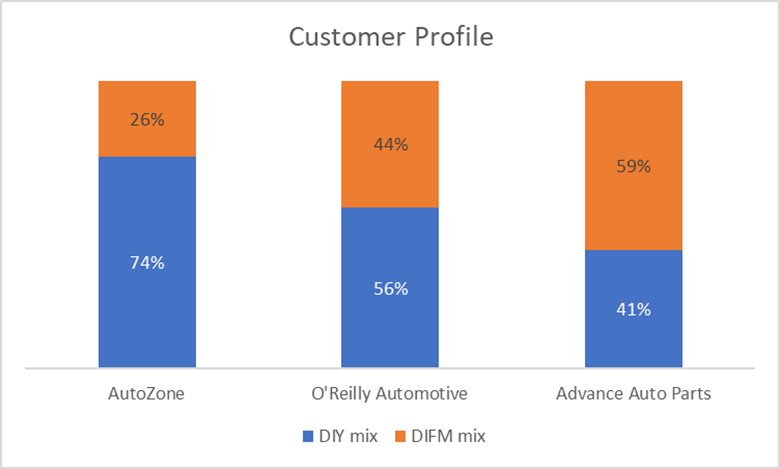

Sales mix by customer types for the 3 companies, from company filing.

Let’s look at it from a customer’s point of view. Again, we have two types: DIY vs DIFM customers.

First are DIY (Do-it-yourself) customers.

DIY customers usually fix the car by themselves. A typical car has over 30K parts, many DIY customers also expect store employees to match the right parts for the right car model, or in some cases even help install the parts. For example, some stores provide free battery testing and replacement, alternator testing, brake testing, wiper installation and even rent you the wrenches to take home so you fix it yourself and bring it back within the next 90 days (AutoZone’s Loan-A-Tool). So, part of that high GP margins is embedded with some level of in-store customer services.

Well, some DIY customers who are more diligent might not want such services. With abundance of online videos available on YouTube and brands having digital catalog sites (see this website for example to find Toyota parts), DIYers could easily look up the right parts online and visit the store afterwards. In fact, all three auto parts players we discussed today have developed comprehensive parts identification systems to easily look up the right part and shot countless YouTube tutorials using its private label parts as replacement demonstration. I guess the issue is more about finding out what went wrong, and here Auto parts retailers are in a bit of an awkward situation since many stores are not equipped with real auto mechanics. Hence some of the common complaints from DIY customers are that the advice given in stores being ineffective.

Annual spending for DIY customers ranged from $100-300, depending on vehicle age, while car owners who prefer DIFM channel spend ~$200-500/year. While some DIY customers are gearheads, many of them have lower income (average household income is 30-75K for DIY vs 50-100K for DIFM), and are more price-sensitive, who do not mind walking over to multiple stores nearby to compare prices. This makes sense since if they are wealthy, they would just drive the car into a repair shop and pay for a mechanic to fix it for them.

But store location and part availability are obviously still big factors, as many people need a car to go to work and make a living, fixing it as soon as possible is still top priority. In the case of engine failure, walking 10 miles to a second store to save an extra 5 bucks for a spark plug when there is one right next to you is not a pleasant task, even for the most price-sensitive group. This is especially true when you know the correct part is right there in the store, but you are not sure you can find it in the next one.

Second are DIFM (Do-if-for-me) customers.

DIFM customers send their orders through phone calls, or an integrated online ordering system linked to these auto part stores. If an auto store is nearby, they would call, request, and walk into the store to pick up the parts within the same day (BOPIS). Otherwise, delivery trucks are dispatched from stores to send parts to them instead.

For this, we need to understand that DIFM customers are always on the clock because having a car stuck inside means opportunity cost from loss revenue from the next job. Auto shops make money by charging customers by the hour for the mechanics ($100-200 / hour) and apply a 20-30% fix mark-up on the parts procured in the process (labor/parts share is about 45/55 split). Hence, once a car is in the bay, they bother less about part procurement cost but more so parts procurement speed. The quicker the car gets fixed and driven out, the faster the space is freed up for the next job, since each mechanic would turn around 3-4 cars per day. Of course, price, speed, relationships, and ease of ordering still matter to them. Garage owners hate it when a previous customer comes back with a misfit part, taking up a precious space without additional income.

Car owners who send their cars to a body shop are generally more willing to spend, which translates to them choosing more expensive parts and should lead to better margins. However, this is countered by generous volume rebate commonly seen in the commercial channel when auto shops purchase parts in bulk, which compress margins for growth.

Net, I think GP margins are still a bit better in DIY than DIFM. Local mom-and-pop auto repair shops are usually more price sensitive, who prefers low prices along with immediate parts availability. The typical lead time for a DIFM customer is around 30 minutes. They want the parts as soon as possible, and they are not afraid to go to the next store website and call their number if the parts have not come in within 30 minutes. In some cases, some DIFM customers even send multiple orders to 2-3 auto part stores simultaneously, and refund/cancel orders that are too slow. In an auto part store, the desks handling commercial customers are known as Commercial Programs and are often placed at the back of the shop.

Apart from the part availability factor, the store manager, also known as a part pro, builds a strong rapport with commercial customers. Each parts pro would know the commercial demand needs well and optimize the store for local part needs, and often refers walk-in customers to send their cars to these auto shops for more complicated parts fix. There are repair shops where they buy from the same auto stores for over a decade simply due to this relationship of the parts pro and garage owner. With not much in-store services, retaining parts pros is key to minimizing customer churns. The industry recognizes that bulk of the future volume growth would come from commercial space, as cars are getting built with more complexity and more and more people are outsourcing car fixes to professionals.

Next, I want to talk about distribution.

Since the name of the game is all about parts availability, supply chain management and parts distribution speed are key success factors. The winners know how to set up stores around a distribution center (DC), how to pick and pack the right parts, how to manage vendor relationships, and establish an efficient logistics system to ensure the right parts are at the right stores at the right time.

Since commercial customers have tight schedules, auto part stores conduct hot shots delivery, a tactic not uncommon in other time-sensitive business, where trucks are dispatched on schedule to deliver parts from nearby hub stores or DC (for items not found in typical stores), directly to repair shops within 30 minutes of parts request (when you call in, you will be added to the mailing list). Once a part is out of the store, it needs to be refilled quickly from the DC to ensure the next customer would enjoy the same speed.

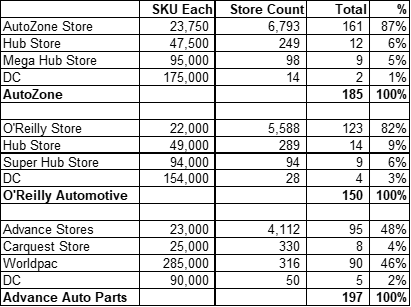

O’Reilly built its distribution strategy mostly around its highly productive distribution centers (28 of them nationwide). Each DC would stock up more than 150K SKUs and could support around 200 stores nearby, where hundreds of workers working hourly shift to pack all the parts requested, and trucks run trips from DC to stores more than once per day (typically, overnight in the morning and in the afternoon).

As for AutoZone, its distribution strategy shifted more burden towards local hub (50K SKUs) and mega hub (90K SKUs) stores as mini warehouses, as it has similar number of stores but with half the DCs compared to O’Reilly, despite the latter having 1.5x in DIFM sales. Here, tractors run trips from DC to stores daily, but a fleet of 250 hub and 100 mega stores replenish nearby stores promptly to ensure customers walking find the right parts on shelf. O’Reilly also has around 300+ hubs and super hubs that are similar SKUs count, albeit they play a smaller role comparatively.

For Advance Auto Parts, its DCs are less inefficient. It has over 50 Distribution Centers with uneven productivity (size ranged from 50K to 1 mil sq ft), and a separate logistics network with larger DCs serving Advance stores and smaller DCs serving Carquest stores and ~1.3K independent stores. For DIFM, orders are often shipped directly from the Worldpac warehouse branches (2x in size and houses over 285K SKUs) to the repair shops. This leads to duplicative logistics infrastructure and overall, less efficiency, issues that I will come back to later. To put it in perspective, O’Reilly DCs serve 200 nearby stores and run 7-10 trips per week, while AutoZone DCs support 500 stores and run 5-7 trips. Advance DCs are trickier to understand. The DCs and Worldpac warehouses supporting Carquest stores are overworked with daily trips while DCs supporting Advance stores run merely 3-4 trips per week.

What a customer sees when walking into an AutoZone store, picture from a YouTube video screenshot.

Let me take you through the history of each player to better understand what led to their current state.

First is AutoZone.

As part of the division of wholesale grocer Malone & Hyde, the first Auto Shack store opened in 1979, and expanded to over 200 stores within next 5 years (as you see later, other guys took a few decades to do that!). From the get-go, the chain was positioned to serve DIY customers (DIY mix accounts for >70 of its current revenue), with colorful well-lit store design, great emphasis on in-store experience/customer services, as a discount part supermarket where you find the right parts easily at lowest price (check out this TV commercial from 1982).

For the next 2 decades, Auto Shack expanded along the Sunbelt/Midwest states, renamed as AutoZone in 1987, being the first Auto chains to be listed in 1991 and reached >1000 stores by 1995. While the colorful store design was unique at that point of time for drawing in demand, supply was carefully taken care of where AutoZone purposefully built its new stores around its network of DCs and hub stores. Such hub stores are 2x in Size and number of SKUs as they were gradually rolled out at the turn of the century to serve as mini-DCs that support neighboring stores to lower the time it takes to ship the parts.

Assortment is carefully curated to suit the needs of DIYers, with sections of the stores divided by clear signage to encourage product discovery. Maintenance items and soft parts are displayed towards the front to attract customer attention, while the hard parts are placed towards the back. Customers walking pass will be lured by its flashy banners and promotions to remind them that it is time to get an oil change or new windshield wipers. AutoZone knows that these failure parts are “destination” items, so they make customers walk all the way to the back to find them, hoping that they pick up an air-refreshers or other discretionary items along, very much like a typical grocery store with the candies being next to the checkout counters. Founder Pitt Hyde III took the retail insight from his family grocery chain – clean, well-organized stores with accessible products and great customer services, and applied it to auto parts stores, and it was a hit because it was nothing like any other stores.

AutoZone acquired ALLDATA in 1996 and launched Z-net as the catalogue look up system in 2008. These catalog systems not only are ways for DIY customers and in-store employees to quickly look up the right parts but provide crucial statistics on parts failure rates for commercial customers to plan for category management. A store would learn from its past data that perhaps radiators are the most common failure causes for cars in Texas due to hot summer, and stock up ample number in anticipation and likewise for dead batteries in Illinois during cold winter, improving fill rate and customer conversion rate.

Although being the last one established, AutoZone led the gain in the 90s, with same store sales growth (SSSG) averaging over 8% while expanding >160 stores organically on average, but slipped up on customer experience that led to weak comps (<1% for 4 years and negative for 2005) during mid-2000s, before it bounced back to comp ~5% on average and opened ~190 stores each year since 2008, and reached ~7K stores in 2023. The key to AutoZone’s strategy is its preference for organic growth over outsized acquisition unlike peers (largest deal was Chief Auto with 560 stores in 1998) which helped to build consistent customer experience, as well as carefully plan new stores opening around its hub stores and distributive network to optimize for most efficient logistics route possible.

Next is O’Reilly Automotive.

The name “O’Reilly” started with Charles O’Reilly. He was selling auto parts for Link Motor Supply for the first half of the 20th century, but the first O’Reilly Automotive store was only established in 1957 from a reorganization of Link. I find it quite interesting that O’Reilly “dual market” strategy, that is serving both DIY and DIFM at the same time, was first mentioned as early as 1978. O’Reilly reached its 100th store in 1989 and got listed in 1993. All along, O’Reilly has pretty much been a story of carefully managed organic growth expansion, until late 90s where it ramped up its acquisition strategy for deals such as Hi/Lo (1998) for its 182 stores in Texas, Mid-State (2001) for its 82 stores in Southeastern States, and Midwest (2005) for its 71 stores across 25 states. Four DCs also came along with these 3 acquisitions, which helped O’Reilly in stretching out its distribution network to further regions. This put O’Reilly as the number 1 chain by store count in Texas (>700 stores) and Missouri (>200 stores) till today. By 2005, O’Reilly had ~1.5K stores (AutoZone had 3.6K and Advance had 2.9K) and ~1.4 mil sales each (about $0.1-0.2 mil below peers), with a 44% GP Margins when peers are at 47-49%.

But the narrative is different now once I told you its 260 stores in 1997 expanded 5x into 2005, while not having any SSSG below 6% except for 2002. But the largest acquisition by far is still CSK’s deal in 2008 where it added ~1300 stores into the network, nearly doubling store count from 1.6K to 3.2K in merely in two years from 2006 to 2008. CSK at that point was made up of 4 auto part chain brands, Checker, Schucks, Kragen and Murray’s Discount, but eventually were swiftly all converted into O’Reilly format within 2 years along with a budget of ~$130K per store to work on inventory shrinkage and integrating IT system and distribution network. This acquisition finally placed O’Reilly as a truly national chain as its presence stretched westward to the Pacific Ocean, with stores in California went from 0 to 480 overnight (likewise for Arizona, Nevada, Washington & Oregon).

The ability to serve both ends of the market means greater flexibility, this means I don’t think all O’Reilly stores have the same formats across America, but management adjust the mix dynamically with each store based on the market conditions. Stores in high density towns have a higher DIY share while less populated areas have higher DIFM mix. Still, on the corporate level, I noticed how consistent management has been in its dual market strategy, carefully managing the mix to balance. The acquisitions of Hi/Lo (65% DIY mix) and CSK (90% DIY mix) has lifted overall DIY shares closer to 60% in different times, just to be brought back down closer towards its intended 50/50 mix in each subsequent periods (current mix is ~55/45). O’Reilly and CSK had minimal store overlap as the combined entity closed only 60 stores (<5%), but more importantly improved utilization rate of DC for dual market needs. After 2008, O”Reilly had then opened up 7 more DCs, improved its retail space per DC square footage by 30%, and increased employee density per DC by 50%. The better utilized DCs were paired with higher delivery network intensity (stores per DC went up from 160 to 210) and route optimization, and enabled O’Reilly to expand its GP margins by 5% since the acquisition and to catch up with AutoZone.

O’Reilly had transformed its IT department with the arrival of CIO Jeff Lauro in 2016 to optimize 1) route density and tracking of trucks, 2) productivity of parts packing within a DC, and 3) pricing and inventory management with POS & vendor integration. While AutoZone builds its IT strategy around customer experiences and excels in flashy catalog/info management systems that encourages item discovery, O’Reilly has a more holistic approach that caters to both ends, with over thousands of employees working in IT departments in ares like data science, analytics, parts demand forecast, price monitoring, etc. The acquisition of CSK pushed up SG&A margins initially by 5% with inefficient store expenses. But management put in the work to remove duplicated cost and improve store worker productivity as well as DC efficiency. Per store sales went up from 1.4 mil in 2009 to 2.4 mil in 2022 (per sq ft sales went up from $200 to $300), while rent only went up marginally from $14 to $15/sq ft and employee count from 12 to 13/store, translated to better fixed cost leveraging and SGA margin dropping from 36% to 31%. I must admit, the growth story of O’Reilly has been quite a sight to observe, seeing that store count 4x to ~6K, per store sales grew 1.5x, and OP margins expanded 10%, over the past 15 years. While AutoZone had pioneered and optimized its hub store network, O’Reilly is the best-in-class at optimizing DCs utilization. But the growth story has not stopped. O’Reilly is still expanding ~200 stores per year by going into smaller rural towns where competition is less intensive.

Last is Advance Auto Parts.

Advance Auto Parts began its root as Advance stores in 1930s, changed to its name in the 1970s to solely focus on auto parts, and reached 100 stores by 1985. Its first major acquisition was getting Western Auto in 1998 from Sears with its 600 Parts America stores. After cleaning up 100 unprofitable/overlapping stores, promptly converting them within 1 year into Advance Auto Stores format. More importantly, this acquisition comes with wholesale distribution network along that supplies DIFM customers, a management goal stated as early as 1996.

Next came the Discount store acquisition in 2002 with 600+ stores, but this time with strong exposure on DIY customers especially in Florida state. Advance used the same playbook to convert these stores and integrate its DCs and gain massive vendor bargaining scales while improving lead times in parts availability. Advance were killing it at this point, expanding stores unit from 650 in 1996 to 2.5K in 2002 while achieving avg 7% in same-store sales growth, resulting in 5x in total revenue. Bear in mind this is happening along with merging new stores and format cleanup, leading to GP margins improvement from 39% to 45%. In 2005, Advance acquired Auto International, a part distributor to continue growing its DIFM segment, shipping parts out directly to car garages from its mega-sized (>300K sq ft) distribution centers.

The last recent major acquisition was General Parts in 2013 with a similar intent of growing its DIFM segment with the remarkable Carquest brands along with ~300 Worldpac warehouse stores. These newly acquired smaller size (smallest at 57K sq ft) 30+ DCs from Carquest are known as “blue” DCs to distinguish from the original mega-sized (largest at ~1 mil sq ft) 10 Advance “red” DCs. I feel like the core issue of Advance post 2002 really comes down to new management then putting the cart before the horse. Advance Auto Parts was just following the same playbook in growing its DIFM presence with each acquisition, expanding its commercial mix from 15% in 2002 to 60% in 2022. But the incremental sales came with declining earnings quality. What we have are some serious integration issues with 4 separate units, Advance, Autopart International, Carquest, and Worldpac, not talking to one another, which led to both internal customer competition and duplicative distributive infrastructure. A professional customer calls into an Advance store, just to find out minutes later that similar parts can be found in a Carquest store nearby with a 10-20% price discount. Carquest and Worldpac were in a much better market position in DIFM than Advance stores that had been DIY-focused but positioned below AutoZone.

Unlike the previous case where Advance were “rescuing” Western Auto from previously failed management, the Carquest and Worldpac had excellent brand recognition and well-designed distribution that outperformed the red stores and DCs. This led it to an awkward situation where you have the smaller acquired entities reluctant to share their distributive capabilities to enhance the bigger corporate entity. Yeah, even though Advance stores do get supply from both red and blue DCs, an incentive issue emerged as shipping parts to a Carquest or Advance store shares the same internal transfer price. It is rational to prioritize blue DCs to ship to Carquest stores and car garages directly to maximize internal P&L. This led to over-utilized blue DCs where workers are complaining about the influx of orders and overworking, while inefficient red DCs are being under-utilized with outdated infrastructure, as shown in its continuous deterioration of ratio of store square footage to warehouse area. Even with a similar number of stores, Advance has 50 DCs compared to O’Reilly’s 28 and AutoZone’s 14.

I mentioned that private label penetration has reached 50%, but this is mostly due to 1) Carquest brand being well-liked among the pro customers and 2) Autopart International importing cheaper foreign parts. Management claimed that private label penetration in DIFM is even higher than DIY, implying a weaker private label penetration on the more DIY-focused Advance stores. But pricing discipline is another issue for DIFM customers, starting with generous rebate on its ~1300 independent stores and car garages to drive e-commerce sales and retain price-sensitive ones when delivery time does not meet competitors. This resulted in lower blended GP margins of 45% despite having brand recognition. Likewise, DIY customers often receive generous coupons to induce them to visit the stores, especially for maintenance and discretionary parts that are not time sensitive. They picked poorer design Advance stores for these cheap deals over the well-lit AutoZone stores or O’Reilly stores with excellent customer services. Advance reached a combined peak store count of ~5400 stores, before shrinking to ~5100 in the next 10 years, despite peers gaining 1K+ stores.

Analysts know it. Management knows it. The integration issue has been repeatedly mentioned in the earning calls, and countless self-help initiatives have been proposed to address these issues. For starters, management implemented a new tech platform in 2020 to improve pricing initiatives and remove unproductive rebates, cleaning up tens of thousands of SKUs across. But the root cause is more strategic than tactical, and it takes much more than this to address its larger issues of supply capabilities and internal conflicts. The 200~ Autopart International stores are finally fully converted into Worlpac format in 2023 after 18 years of being acquired (recall O’Reilly took 2 years for ~1300 CSK stores). Management closed a DC in San Antonio in 2018, while acknowledging that having >50 DCs serving different brands is too inefficient. The number of DC did shrunk by 4 over the next few years, and other pilot programs and attempts to integrate emerged in Illinois and Tennessee DCs, but concrete progress hasn’t been made until 2022. Advance Auto Parts combined Carquest and Wordpac in Ontario to a much larger DCs (580K sq ft and holds 350K SKUs) supporting 130 Carquest stores and 37K auto shop customers nearby.

Part of the issue was a lack of management experience in the auto sector. Among the previous CEOs, Tom Greco (2016-2023) came from Pepsi and Darren (2008-2016) came from Best Buy. But I do like the new CEO Shane O’Kelly with HD supply and more importantly, over 6 years of experience in lubricant distributor PetroChoice. At last, we have a real auto guy running the business. O’Kelly joined in September 2023 and promptly initiated a sale for the Worldpac and Canadian business while he admitted that an independently run Worldpac does not fit well in serving DIY customers. Recognizing the margin gap from peers, he is bringing in Ryan from Lowe’s (sadly no auto experience too) as CFO and announced a $150m cost reduction program from simplifying operation along with $50m reinvestment back to higher wages and training (mostly towards retaining parts pro, I guess). The new CEO is looking to get Advance back to profitable growth, aiming for OP margins improvement to start in 2024. But I think the most important aspect by far is his plan on rationalizing unproductive DCs and overhauling the entire logistics system, aiming for a unified supply chain for the entire company. Unfortunately, recent calls provide little details as to how it can be executed, and crucially what do they do now differently than before.

I would like to benchmark the three firms and see how they have done over the years.

Despite operating around the same number of 6-7K stores, with similar store sizes of 6-8K sq ft, and serving roughly the same needs from customers, the performance outcome cannot be more different in the last decade. This is why I find this industry so interesting. The Auto part national chains are sometimes referred to as Big 4, with NAPA (listed as Genuine Parts) being the fourth player with its ~6K stores. I excluded NAPA in this analysis because its business mix is not as clean (it also has an industrial distribution business) and it operates on a network of 5K independent franchisees, a model that is not appealing to me in this industry (Although Advance Auto Parts also has around ~1.5K independent stores brand as Carquest). To give you a perspective on the business performance divergence, look at the following operating metrics on the three players.

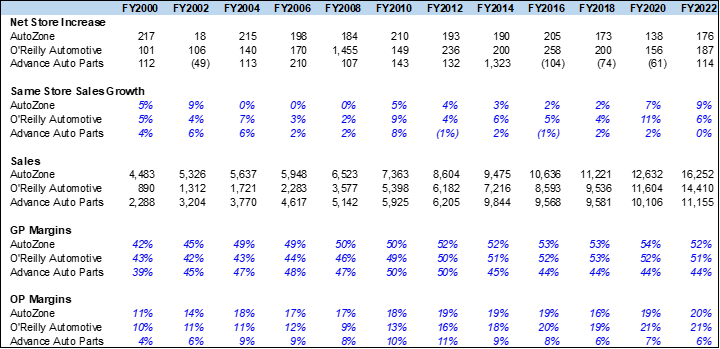

Sales and margin trend compared; data computed from company filings.

We can attribute the 14% OP margin gap on Advance to 1) 8% GP margin gap from inefficient distributive network and weak vendor bargaining power where they often have three separate parties negotiating with the same vendor, 2) 6% SGA margin gap from ~2% in higher rental share of square footage (85% compared to 55-60%) and ~4% in cost inefficiencies stemmed from lack of IT system integration and duplicative back-end costs. On the latter point, I realized that per sq ft rent is about the same for all 3 cos at ~15/sq ft, so the difference in cost comes down to how much floor space is rented as opposed to owned & depreciated away. Advance also lacks flexibility when it comes to coordinating its share of rental space, maintaining it at 82-85% for the last 15 years. AutoZone’s rental share of square footage has gone up 10% to 55% in the last 15 years while O’Reilly has lowered its share by 10% to 60%.

To be fair, since auto part stores enjoy higher margins, the weak IC turns is a bigger factor than the margin difference here. From the vendor point of view, given that they have high operating leverage, what they care about is plant utilization rate, so auto part retailers serve a role in producing accurate forecasts for them to plan their production lines. In other words, vendors want order visibility in exchange for better pricing and longer payment terms for the retailers. The longer days do not bother them as long as sales are certain, they can always factor their receivables when they need cash. Thus, the long payable days offset the high inventory count, enabling AutoZone and O’Reilly to achieve working capital at -20% of sales. This may seem strange at first. Unlike Walmart, which achieves negative working capital with high turnovers in both inventory and payables, auto retailers do the opposite.

The key here is to recognize not just inventory days but inventory quality. Holding a large inventory makes sense if you can with strong supplier support mentioned earlier that enables high payable days to lower working capital along. As a result, O’Reilly has improved its payable days from 120 days to over 300 days. AutoZone cares less about payment terms and more about cost containment, requiring its vendors to notify them within 90 days of any cost increase. Advance Auto Parts has suffered from weaker bargaining power that is mostly attributable to their poor execution in being too passive and reactive. The key to assessing working capital is not just cash conversion cycles but also inventory to payables ratios, where AutoZone and O’Reilly have reached 1.3x, while Advance Auto Parts suffered with only 0.6x.

Part supplies could come from both OEM and remanufacturers. Remanufacturing is taking a core part and refurbishing it into new conditions for parts replacement, and finding a core to replace is not easy, adding uncertainty to the planning process. AutoZone has a highly integrated IT system that can generate timely forecasts from each of its 10 national DCs and feed right into suppliers, who then take only a lead time of 7 days to produce and deliver the necessary parts. Advance Auto Parts and NAPA both operate franchise/independent models which come with the competitive disadvantage of franchisees not carrying enough inventory and not being trusted by vendors on the forecast. Such forecast numbers are less accurate without firm-wide information coordination unlike AutoZone and O’Reilly.

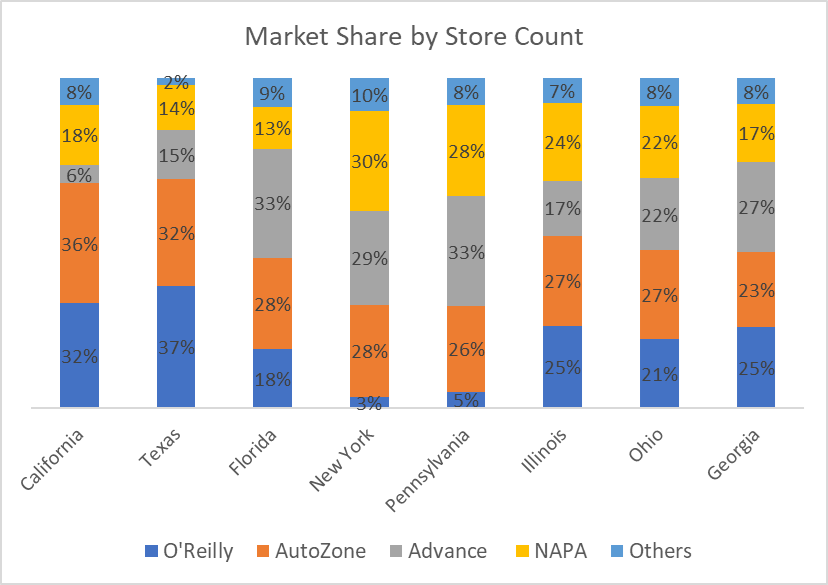

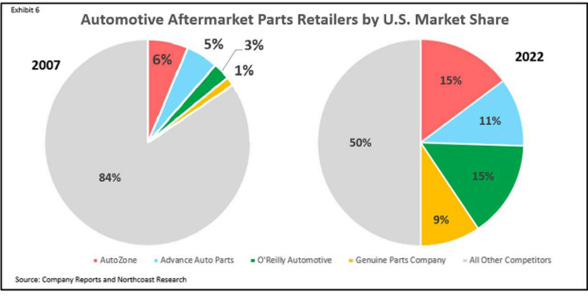

After market share by channel, from Advance Auto Part’s Investor Presentation in 2021.

The TAM for DIY is ~$75B while DIFM is a ~$115B industry. Total market size expands only at 3-4% for this mature industry, but opportunities for rollup exist within the space. While DIY is more consolidated, DIFM is fragmented where 1) auto parts store to take share from dealers (16% of TAM) as cars out of warrant opt for independent auto shops for cost saving, and 2) taking share from thousands of local mom-and-pop auto parts stores serving their local town needs. Among the ~40K auto part stores in the US, the 4 national chains only account for about ~50% of store share (less than 20% of value share in DIFM).

The tailwind in this space has been the natural chain stores consolidation over time with each players exploring new markets town by town, driving out local competition with their superior distribution network and comparatively lower price driven by scale economics. These local shops usually have no choice but to give in by being acquired by one of the larger chains to survive. The parts availability is such an important that auto parts chains still gain market shares over independent despite surveys showing a 10-20% price premium gap between both on at least 1/5 on the category. Each of these players is regionally dominant2 but we can see the consolidation from national market share trends as well. O’Reilly 3x both its DIY/DIFM share within the last 15 years to 10% and 5%, AutoZone kept its DIY share at 15% and grew DIFM share to 3%, while Advance lost market share.

There is sufficient gap between the top players to discourage the rest from trying. In 2016, Carl Icahn acquired Pep Boys to disrupt the market by sourcing from its own distributor AutoPlus with lower price. Pep Boys is the fifth largest chain with ~1K stores, it also offers tire & repair services and competes against its customers. But after a few years, Icahn slowly gave up on the parts business to focus more on services and tires. Burdened with debt, the auto part stores were spin out as Auto Plus Auto Parts and filed for chapter 11 in 2023.

Short term trends for car part replacement are driven by weather conditions. Rainy days tend to have more windshield wiper replacement, and hot weather would attract demand for battery sales and oil change, while snowy weather would drive more sales for anti-freeze and windshield washer.

But over the longer term, total miles driven in American went up from 2.2 trillion in the 90s to 3.2 trillion miles now, driven by both more and higher utilization of cars. The older cars, despite being driven less per year, are more prone to have broken parts, and more likely to be sent to a garage shop. The average age of the car fleet has also gone up from 7 years in the 80s to 12 years now, as cars are better built, and people keep their car for longer. The sweet spot of the ideal car age lies beyond 5 years where a car is out of warranty but not more than 11 years where a car owner starts to think about switching to a new one.

I suspect that the percentage of parts related to failure parts is probably higher in DIY sales than a DIFM sale, given that DIY customers hold onto their cars for longer, while their annual spending goes up rapidly from $100-150 to $250 and above after year 16, while DIFM customers spending peak at $500 after year 6 and trends down afterwards.

Since 2006, the TAM per Vehicle in Operation has gone up from $470 to $680, driven up by larger share of cars within this sweet spot range (share of aged 5+ cars went up from 65% in 2006 to 80% now). This correlation of miles driven, and failure rate is quite strong where it charts a straight line to the right and top. With cars being built with better quality, the y-intercept does shift higher and the line being less steep and longer over time. In the 1970s, cars often did not make it pass 100K miles, now survey showed 2/3 of cars driven passed that mark. Going forward, DIFM will grow a bit faster because cars are made more complex, driving people to send them to a repair shop equipped with trained mechanics to handle parts complexity.

E-commerce poses a threat to mostly maintenance and discretionary parts, such as planned brake jobs, air-refreshers, and car wax, but it won’t disrupt failure-prone parts (e.g. engines, alternators, starters, and chassis). Putting aside the issue of longer wait time, consumers usually want OEM brands for these failure parts as they demand quality, and Amazon is probably not the distribution channel in mind for OEMs. Rock Auto, on the other hand, managed to secure quite some OEM sourcing over the years as they borrowed the merchant strategy from off-price stores and became the dumping ground for unsold/overproduced parts (an unglamorous truth for these OEM brands actually).

What about distribution? If it comes down to an efficient delivery mechanism, doesn’t that sound like something that Amazon could emulate?

First, I do acknowledge that Amazon can achieve same day delivery for many parts (mostly urban though) of America, but DIFM is asking for less than 30 minutes in many cases and Amazon is not going out of its way to achieve that.

Second, delivering the parts fast can become a weakness if you send the wrong parts, since Amazon does not have parts pro to ensure right parts and maintain car garages’ relationships (remember, auto stores are their best friend because parts bottleneck is a big deal), Amazon is not going to win in the DIFM space. As for DIY sales, you can’t replace a broken windshield wiper by ordering from Amazon and wait 1-2 days while you are sitting in the car with rain outside. You would rather drive to a nearby AutoZone store and have the store employees installed for you immediately. Amazon does not have staff in a store to trial and fit the parts for the buyers. When there is something wrong, mailing back the parts and getting a replacement is a pain in the ass.

This contrasts with an AutoZone where you have in-store people who help a DIYer, diagnostic, test and install parts all on the spot, and customers walk out worry-free knowing that the parts would work for sure. AutoZone and O’Reilly simply have more inventory at the store front that is closer to customers, and they can get the parts within 1-2 hours from a nearby hub store for any missing part. While Amazon, no matter how low its prices are, simply is not matched in both the service and speed of sending car parts. Carparts.com is a publicly listed online car parts platform, but it relies on third party logistics infrastructure to ship parts from its own DC and uses a drop-ship model (shipped from auto parts warehouse to customers) for other parts. It claims 24-48 hours delivery time, but the reality is waiting time depends on how fast a FedEx or UPS takes to ship to a customer, where it could take anywhere from 1-5 days. Carparts.com has about $600-700 million in sales. It is not surprising that ~70% of products sold are replacement parts (mostly maintenance and discretionary items) and only ~30% are in hard parts (mostly failure parts).

Without in-store services and immediate parts availability, the auto part business model is no longer of high-quality. Carpart.com only fetches 35% in GP margin even with ~90% house brands, and barely makes profits with <1% OP margins. Rock Auto has a similar business model. It has a fanciful online store with a large assortment, but parts are delivered by FedEx and UPS. I can hardly imagine them winning the more profitable share of demand in this industry. Therefore, ecommerce is likely to retain a smaller share of total revenue, somewhere between 10-20%.

Electric Vehicles (EV) are powered by battery instead of an internal combustion engine (ICE), reducing the typical 30,000-part car down to less than half. As a result, the potential TAM for aftermarket would shrink massively, with as much as 40% of SKUs from an auto part will go obsolete as EV needs no exhaust systems, alternators, fuel injectors or starters, but more cameras, sensors, and other electronics. EV still share some similar parts with ICE, such as brake pads, mirrors, and windshield wipers, but the issue is that huge chunk of failure parts in an ICE went missing in its electric counterpart, and those failure parts as mentioned earlier are the real profit drivers for auto part stores. While batteries are used in EV as the most crucial component, they are nothing like the ones used in a gas-powered car when it comes to design and energy density. With more complexity and technology built into newer cars (cars are increasingly thought of as iPhone on wheels now), this would further drive-up sales for DIFM customers who develop more niche knowledge on specific brands and more complex part replacement.

The attitude of EV OEMs towards aftermarket parts is unlike traditional OEMs where they may extend the service and parts replacement well beyond warranty years. Tesla is known for its close system philosophy and tight control on value chain, perhaps inspired by Apple who has similar obsession on product quality control. Tesla performs diagnostics remotely via software, and proactively schedules service appointments with its ~190 service centers, ~1700 Collision Center, and ~1800 Mobile Service fleet, so to prevent the car being sent to a car garage or auto shops. Likewise in distribution, Tesla wants to ditch the network of dealers and sell directly. Knowing this, more auto stores choose not to stock many Tesla parts, with many shops having no parts at all. Tesla does make money from its software and after-service, with a friend of mine who drives one showing me that its software subscription could cost up to a few hundred per month. When asked about it, industry people often dismiss EV as a distant threat. With a global new sales penetration of 10% (less than 1% for current fleet) and an average fleet age of merely 3-4 years, it would take at least 1-2 decades to build up the fleet, giving ample time for auto stores and car garages to shift their inventory mix. In response to EV brands insourcing aftermarkets, lawyers push for Rights to Repair acts to force market competition. So, EV remains a minor threat for now.

AutoZone has bright store designs, consistent DIY experience and efficient distribution system, and it derived growth for the last 2 decades organically. O’Reilly is more capable in acquisition and integration and has shown execution track record on dual markets, built its fast logistics network around its well-optimized DCs, and likely to take more DIFM shares from peers. Advance struggled with price management, under-utilized assets and lack of integration, but it has decent recognition from its Carquest brands.

Above-market returns are generated from finding turnaround cases (those where ROIC improved from worst to best) or quality businesses at a discount (getting into a high ROIC business at a discount price and sitting with it for years).

Advance Auto Parts’ fit the former and probably appeal to someone looking for much higher returns if the company does turnaround. A more serious investor would probably visit a few Advance/Carquest stores in the US, talk to their employees and customers, and dig out more on what management really plan to do to address its distribution issue to sense a more accurate probability of success. But I don’t live in the US, I don’t have contacts to reach out to, and hell I don’t even know how to drive a car to be honest. So, the case is too hard for me. Results are too binary. The upside/downside scenario is too hard a call for me to make.

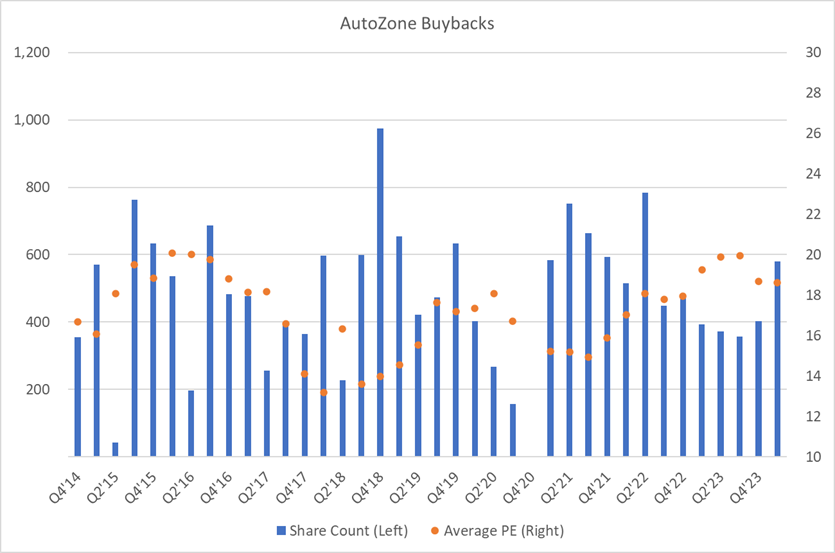

As for AutoZone and O’Reilly, the key driver for top-line growth is consistency in finding places around their fast distribution system with limited competition (mostly local shops), achieving ~200 store growth (3-4% per year) and 5-7% SSSG at the same time, so revenue grew about 8-11% each year. On top of that, O’Reilly had a 15-year margin expansion from 10% to 20%, share bought back that cut share count by half (~7% EPS growth contribution), its EPS grew 22%. AutoZone’s margin only expanded 2% but its share buyback activities reduced share count from 60 million to 20 million, boosting EPS growth to 19%. For AutoZone EPS growth would have been halved without such buybacks. Its lower growth prospects and perceived financial engineering with aggressive buyback shunned some investors away, hence AutoZone has consistently been valued at 5-8x gap compared to O’Reilly. Multiples for both players hovered around teens to mid-20s, and only experienced temporary dip around 2017 when the industry was faced with an Amazon disruption scare. Going forward, given say a fair multiple of 16x/20x is given to AutoZone/O’Reilly, and let’s say continue this 200 store/year expansion & 5% SSSG trend, along with 0.5% margin expansion per year, and we assume they both buys back 75% of operating cash flow. O’Reilly yields a 5% IRR while AutoZone would get a 12% IRR (of which 6% are from buyback). I do own a small amount of AutoZone in my portfolio. Given that buyback activity is rather programmatic (see note 3 below on buyback amount and P/E), even a dip in valuation would mean higher share count reduced, pushing up EPS anyway. I acknowledge that O’Reilly has better growth aspects with its better positioned DIFM execution, but its 27x multiple is putting me off waiting for better opportunity.

AZO 0.00%↑ ORLY 0.00%↑ AAP 0.00%↑

Notes: